Free Promissory Note Form

Simple PDF Forms

Free Promissory Note Form

Understanding a Promissory Note is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are ten common misunderstandings about Promissory Notes:

By clarifying these misconceptions, individuals can better navigate the lending and borrowing process, ensuring that their financial agreements are clear and enforceable.

Once you have your Promissory Note form ready, it’s important to fill it out accurately to ensure that all necessary information is included. This form will serve as a binding agreement, so careful attention to detail is essential. Below are the steps to help you complete the form correctly.

After completing these steps, review the form carefully to ensure all information is accurate and complete. Once you have confirmed that everything is in order, you may proceed with any additional steps required for your specific situation, such as notarization or filing, if necessary.

Filling out a Promissory Note form can seem straightforward, but several common mistakes can lead to complications. One frequent error is failing to clearly state the loan amount. If the amount is ambiguous or incorrectly written, it can create disputes later on. Always ensure that the numerical figure and the written amount match precisely to avoid confusion.

Another common mistake is neglecting to include the date of the agreement. Without a date, it becomes difficult to determine the timeline for repayment or any applicable interest rates. Including a clear date helps establish the terms of the loan and provides a reference point for both parties.

People often overlook the importance of specifying the repayment terms. Vague language regarding when and how payments will be made can lead to misunderstandings. It is crucial to outline whether payments will be made monthly, quarterly, or in a lump sum, along with any grace periods or late fees.

Signing the document incorrectly is another pitfall. All parties involved must sign the Promissory Note for it to be legally binding. If a signature is missing or improperly executed, the note may not hold up in court. Double-check that everyone has signed and that their names are printed clearly beneath their signatures.

Some individuals fail to include the interest rate or mistakenly write it down. This omission can lead to confusion about the total amount owed over time. Clearly stating the interest rate, whether it is fixed or variable, ensures that both parties understand their financial obligations.

Lastly, neglecting to keep a copy of the signed Promissory Note can create significant issues. Without a copy, one party may claim terms that differ from what was agreed upon. It is essential to retain a signed copy for personal records, ensuring that both parties have access to the same information.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a defined time or on demand. |

| Parties Involved | There are typically two parties involved: the maker (who promises to pay) and the payee (who receives the payment). |

| Governing Law | The Uniform Commercial Code (UCC) governs promissory notes in most states, but specific state laws may also apply. |

| Interest Rates | Promissory notes can include interest rates, which can be fixed or variable, depending on the agreement between the parties. |

| Enforceability | For a promissory note to be enforceable, it must be signed by the maker and contain clear terms regarding payment. |

| Types | There are different types of promissory notes, including secured and unsecured notes, which differ in terms of collateral. |

A Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a certain time or on demand. It serves as a legal document that outlines the terms of the loan, including the amount borrowed, interest rate, repayment schedule, and any penalties for late payments.

Individuals and businesses commonly use Promissory Notes. They can be utilized in various situations, such as personal loans between friends or family, business loans, or real estate transactions. Both lenders and borrowers benefit from having a clear record of the terms agreed upon.

A well-drafted Promissory Note should include:

Yes, a Promissory Note is legally binding as long as it meets certain criteria. Both parties must agree to the terms, and the document must be signed. It is advisable to have the document notarized to add an extra layer of authenticity. If either party fails to adhere to the terms, the other party can take legal action to enforce the agreement.

A Promissory Note is a vital document in lending agreements, outlining the borrower's promise to repay a loan. However, it is often accompanied by several other forms and documents to ensure clarity and legal protection for both parties involved. Here are some commonly used documents that complement a Promissory Note:

Understanding these documents can help both lenders and borrowers navigate the lending process more effectively. Each plays a crucial role in ensuring that all parties are aware of their rights and responsibilities.

Paper Prescription - Document medication concerns to discuss with your provider effectively.

When engaging in a motorcycle sale, it is essential to utilize the proper documentation, such as the Oregon Motorcycle Bill of Sale form. This not only ensures that the transaction is recorded accurately but also streamlines the process of transferring ownership. For your convenience, you can find reliable Vehicle Bill of Sale Forms that simplify this important procedure, enabling a legally sound transfer.

Letter of Reccommendation - Fosters innovation by encouraging diverse thoughts and ideas.

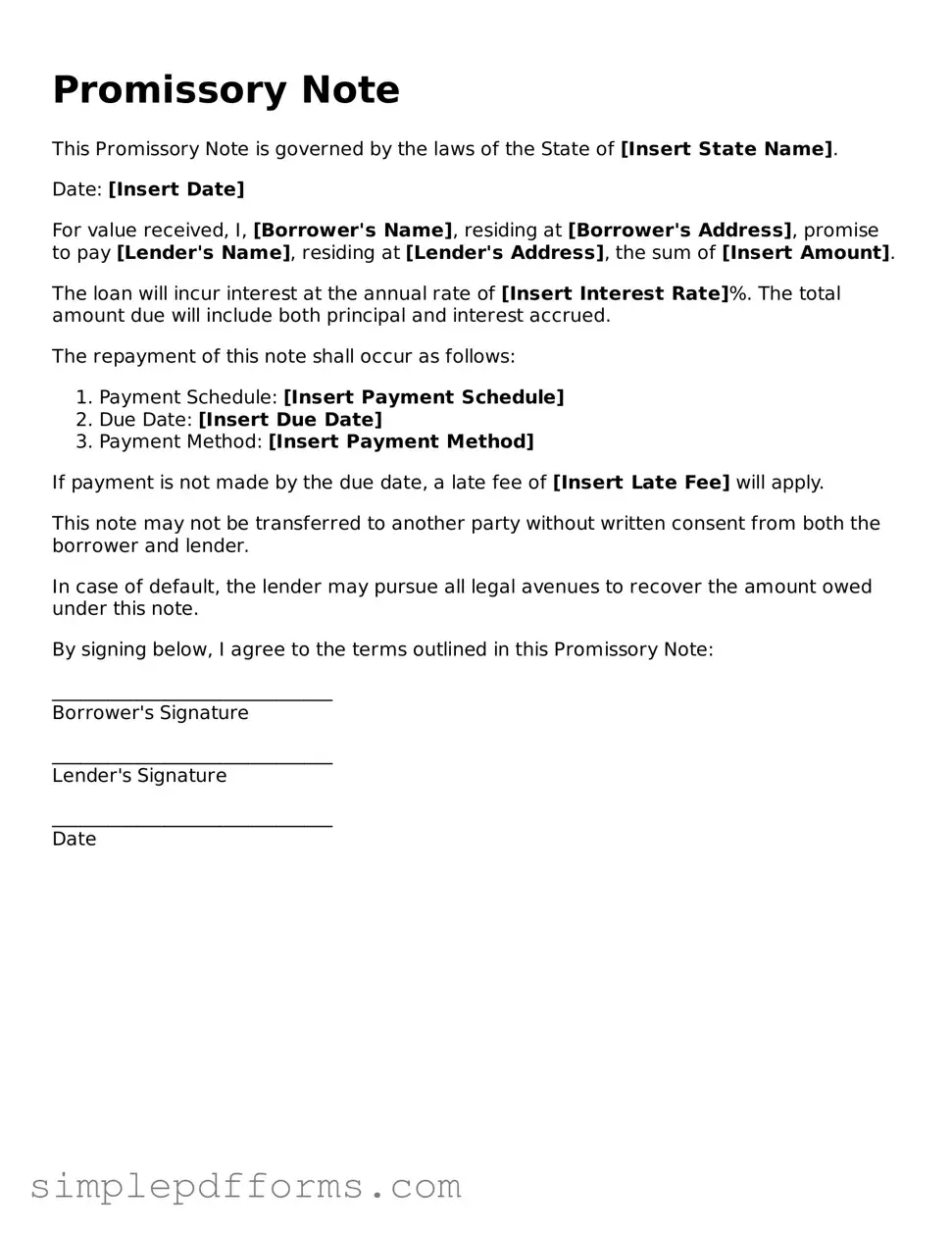

Promissory Note

This Promissory Note is governed by the laws of the State of [Insert State Name].

Date: [Insert Date]

For value received, I, [Borrower's Name], residing at [Borrower's Address], promise to pay [Lender's Name], residing at [Lender's Address], the sum of [Insert Amount].

The loan will incur interest at the annual rate of [Insert Interest Rate]%. The total amount due will include both principal and interest accrued.

The repayment of this note shall occur as follows:

If payment is not made by the due date, a late fee of [Insert Late Fee] will apply.

This note may not be transferred to another party without written consent from both the borrower and lender.

In case of default, the lender may pursue all legal avenues to recover the amount owed under this note.

By signing below, I agree to the terms outlined in this Promissory Note:

______________________________

Borrower's Signature

______________________________

Lender's Signature

______________________________

Date