Fill a Valid Profit And Loss Form

Simple PDF Forms

Fill a Valid Profit And Loss Form

The Profit and Loss form is a crucial document for businesses, providing a snapshot of financial performance over a specific period. However, several misconceptions can cloud its importance and utility. Here are six common misunderstandings:

Many believe that only big corporations need to worry about a Profit and Loss form. In reality, every business, regardless of size, can benefit from tracking income and expenses to understand its financial health.

Some people think that the Profit and Loss form provides a complete picture of cash flow. However, it focuses on revenues and expenses, not the actual cash on hand. For cash flow insights, a separate cash flow statement is necessary.

There’s a common belief that these two financial documents are interchangeable. While both are essential, the Profit and Loss form summarizes income and expenses over time, while a balance sheet provides a snapshot of assets, liabilities, and equity at a specific moment.

Many assume that the Profit and Loss form is solely for tax filings. In truth, it serves as a valuable tool for internal decision-making, helping business owners assess profitability and identify areas for improvement.

Some people shy away from the Profit and Loss form, thinking it is too complex. While it does contain numbers and financial terms, with a little guidance, anyone can learn to read and interpret it effectively.

Lastly, there is a misconception that the Profit and Loss form only looks backward. While it does report on past performance, it can also help in forecasting future trends and making informed business decisions.

By dispelling these misconceptions, business owners can better appreciate the value of the Profit and Loss form in managing their financial health and driving growth.

Completing the Profit and Loss form is an essential step in understanding the financial performance of your business over a specific period. By accurately filling out this form, you will be able to assess your revenues, expenses, and ultimately your profitability. Below are the steps to guide you through the process of filling out the form.

Filling out a Profit and Loss form can be a straightforward task, but many people make common mistakes that can lead to inaccurate financial reporting. One frequent error is failing to include all sources of income. Individuals often overlook additional revenue streams, such as freelance work, side businesses, or passive income. This omission can distort the overall picture of financial health, leading to misguided decisions.

Another mistake occurs when expenses are misclassified. People sometimes categorize expenses incorrectly, which can affect tax reporting and financial analysis. For example, personal expenses might be mistakenly recorded as business expenses. This not only complicates the financial statements but can also raise red flags during audits.

Additionally, many individuals neglect to update their Profit and Loss form regularly. Financial situations can change frequently, and failing to keep the form current can result in outdated information. Regular updates are essential for making informed business decisions and ensuring that financial reports reflect the most accurate data.

Lastly, some individuals do not maintain proper documentation to support the entries made on the form. Without receipts, invoices, or other records, it becomes challenging to verify the accuracy of the reported figures. This lack of documentation can lead to confusion and disputes, especially if questions arise during tax time or financial reviews.

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form summarizes a business's revenues, costs, and expenses over a specific period, providing insight into financial performance. |

| Components | This form typically includes sections for gross revenue, cost of goods sold, operating expenses, and net profit or loss. |

| Frequency | Businesses often prepare this form monthly, quarterly, or annually to track financial health. |

| State-Specific Forms | Some states require specific formats or additional information, governed by state laws such as California Corporations Code Section 220. |

| Tax Implications | The information on the Profit and Loss form is crucial for tax reporting, as it affects taxable income. |

| Analysis Tool | Business owners use the form to analyze trends, make informed decisions, and identify areas for improvement. |

A Profit and Loss form, often referred to as an income statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period. It provides a clear picture of a business's financial performance, showing whether it has made a profit or incurred a loss over that time frame.

This form is crucial for several reasons. First, it helps business owners and stakeholders understand the company's profitability. Second, it aids in financial planning and budgeting by highlighting areas where costs can be reduced or revenues increased. Lastly, it is often required by lenders and investors to assess the financial health of a business.

The main components of a Profit and Loss form include:

Typically, businesses prepare a Profit and Loss form on a monthly, quarterly, or annual basis. Monthly reports allow for close monitoring of financial performance and timely adjustments. Quarterly reports provide a broader view, while annual reports are essential for long-term financial analysis and tax purposes.

Yes, the Profit and Loss form is often used when filing taxes. It provides the necessary information about income and expenses, which tax authorities require to determine taxable income. Accurate records in this form can help ensure compliance with tax regulations.

While both documents are essential for understanding a business's financial health, they serve different purposes. The Profit and Loss form focuses on performance over a specific period, detailing income and expenses. In contrast, a balance sheet provides a snapshot of a company's financial position at a specific point in time, showing assets, liabilities, and equity.

Analyzing a Profit and Loss form involves looking at key metrics such as gross profit margin, operating profit margin, and net profit margin. Comparing these metrics over time can reveal trends in profitability. Additionally, benchmarking against industry standards can help assess whether the business is performing well relative to its competitors.

The Profit and Loss form is a crucial document for assessing a business's financial performance over a specific period. However, it is often accompanied by several other forms and documents that provide a comprehensive view of the company's financial health. Below is a list of commonly used documents that complement the Profit and Loss form.

Utilizing these documents alongside the Profit and Loss form can enhance financial analysis and decision-making. A comprehensive understanding of all financial aspects is essential for the successful management of any business.

Western Union Money Transfer Receipt PDF - Transfer funds to friends or family effortlessly.

Official Cuddle Buddy Application - Join cuddle sessions to encourage emotional openness.

Odometer Statement Indiana - The Notary's commission expiration date is noted for additional verification.

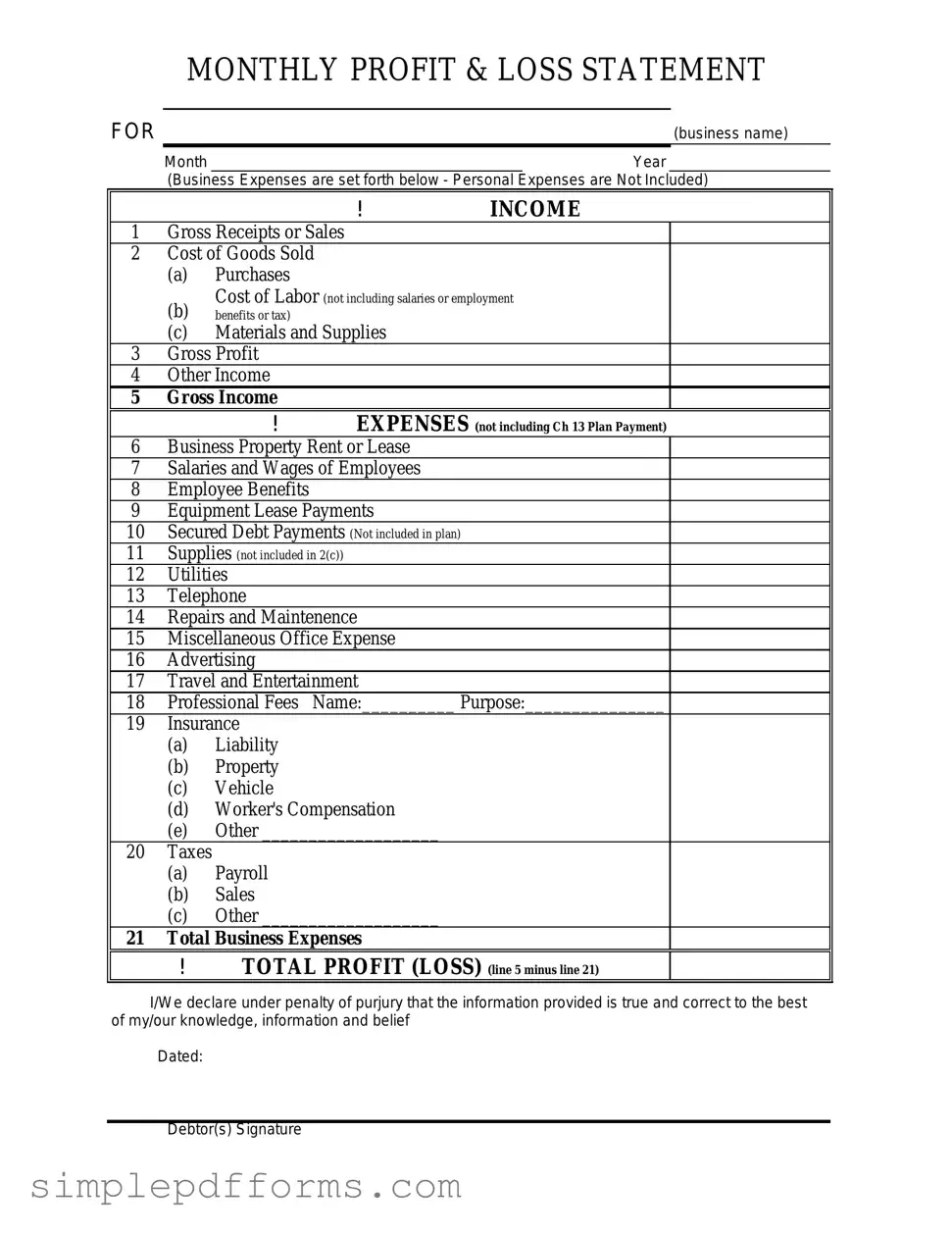

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature