Attorney-Verified Deed in Lieu of Foreclosure Document for New York State

Simple PDF Forms

Attorney-Verified Deed in Lieu of Foreclosure Document for New York State

Understanding the New York Deed in Lieu of Foreclosure can be challenging. Here are ten common misconceptions about this legal process:

After completing the New York Deed in Lieu of Foreclosure form, the next steps involve submitting the document to the appropriate parties and ensuring that all necessary signatures are obtained. This process may require coordination with your lender and possibly legal counsel to ensure compliance with state laws and regulations.

Filling out the New York Deed in Lieu of Foreclosure form can be a daunting task for many homeowners. A common mistake is not fully understanding the implications of this legal document. A deed in lieu transfers ownership of the property back to the lender, which can affect your credit score and future borrowing capabilities. Therefore, it is crucial to comprehend the long-term consequences before proceeding.

Another frequent error involves incomplete information. Homeowners may overlook essential details, such as the property address or the names of all parties involved. Missing even a single piece of information can lead to delays in processing the deed, and in some cases, it may even render the document invalid.

Some individuals fail to provide accurate legal descriptions of their property. This description should be precise and match the information on the original deed. A vague or incorrect legal description can create confusion and complicate the transfer process, leading to potential legal challenges down the line.

Not consulting with a legal professional is another mistake that many make. While it may seem like a straightforward process, legal nuances can arise. A qualified attorney can provide invaluable guidance, ensuring that all aspects of the deed are properly addressed and that the homeowner's rights are protected.

Homeowners sometimes neglect to communicate with their lenders. Keeping the lender informed about the intention to pursue a deed in lieu can facilitate a smoother process. Failure to do so may result in misunderstandings or unexpected complications, such as additional fees or penalties.

Another pitfall is not reviewing the terms of the mortgage agreement. Homeowners might overlook specific clauses that could affect their ability to execute a deed in lieu. Understanding these terms can prevent unexpected hurdles and ensure that the process goes as smoothly as possible.

Additionally, some individuals may rush through the signing process. Taking the time to read the document thoroughly is essential. Rushing can lead to mistakes or misinterpretations that could have been easily avoided with a careful review.

Many homeowners also forget to obtain a copy of the completed deed. After the document is signed and submitted, it is crucial to keep a copy for personal records. This serves as proof of the transaction and can be important for future reference.

Another common error is failing to consider tax implications. A deed in lieu of foreclosure may have tax consequences that homeowners are unaware of. Consulting with a tax professional can help clarify any potential liabilities, ensuring that individuals are prepared for what lies ahead.

Finally, some homeowners may not fully understand the impact on their credit score. While a deed in lieu may be less damaging than a foreclosure, it still affects creditworthiness. Being aware of this impact can help individuals make informed decisions about their financial future.

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal agreement where a borrower voluntarily transfers the title of their property to the lender to avoid foreclosure proceedings. |

| Governing Law | This process is governed by New York State Real Property Actions and Proceedings Law (RPAPL) and other relevant statutes. |

| Benefits | One key advantage is that it can help borrowers avoid the lengthy and costly foreclosure process, allowing for a quicker resolution. |

| Considerations | Borrowers should be aware that a deed in lieu may still impact their credit score and should consult with a financial advisor before proceeding. |

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to voluntarily transfer ownership of their property to the lender. This option is typically pursued when the homeowner is unable to keep up with mortgage payments and wants to avoid the lengthy and stressful foreclosure process.

How does the process work?

The homeowner initiates the process by contacting their lender to express interest in a Deed in Lieu of Foreclosure. The lender will review the homeowner's financial situation and the property's value. If both parties agree, the homeowner signs the deed, transferring ownership to the lender, who then releases the homeowner from the mortgage obligation.

What are the benefits of a Deed in Lieu of Foreclosure?

Are there any drawbacks?

While there are benefits, there are also drawbacks to consider. The homeowner may still face tax implications if the lender forgives any debt. Additionally, not all lenders accept Deeds in Lieu, and homeowners may need to demonstrate financial hardship to qualify.

What is the impact on credit scores?

Generally, a Deed in Lieu of Foreclosure is less damaging to a credit score than a foreclosure. However, it may still negatively affect the score, depending on the homeowner's overall credit history and how the lender reports the transaction.

Can I still qualify for a mortgage after a Deed in Lieu?

Yes, it is possible to qualify for a mortgage after a Deed in Lieu, but it may take time. Lenders typically require a waiting period, which can range from two to four years, depending on the lender's policies and the homeowner's financial situation.

What should I do if I am considering this option?

Consulting with a real estate attorney or a housing counselor can provide valuable guidance. They can help you understand the implications of a Deed in Lieu and assist you in negotiating with your lender. It’s important to fully understand your options before making a decision.

A Deed in Lieu of Foreclosure is a useful document for homeowners facing foreclosure. It allows the homeowner to transfer ownership of the property back to the lender in exchange for the cancellation of the mortgage debt. However, there are other important forms and documents that often accompany this process. Here’s a list of six common documents that you may encounter.

Understanding these documents can help homeowners navigate the deed in lieu of foreclosure process more effectively. Each plays a significant role in ensuring that the transition is as smooth as possible.

Will I Owe Money After a Deed in Lieu of Foreclosure - The homeowner must vacate the property, which may involve timing and planning issues.

The Arizona Non-compete Agreement form is essential for employers looking to safeguard their business interests. By implementing this legal document, businesses can restrict employees from engaging in similar professional activities in certain geographical areas for a defined period after their employment ends. Such measures help maintain a competitive edge by preventing the misuse of proprietary knowledge and trade secrets. To streamline this process, you can find the necessary template by visiting Arizona PDF Forms and ensure that your business is adequately protected.

Will I Owe Money After a Deed in Lieu of Foreclosure - This form may include specific conditions that the borrower must meet.

Deed in Lieu of Foreclosure Pennsylvania - It's advisable to review personal circumstances and available options comprehensively.

Foreclosure Vs Deed in Lieu - Homeowners should ensure all conditions are documented in writing to avoid misunderstandings later.

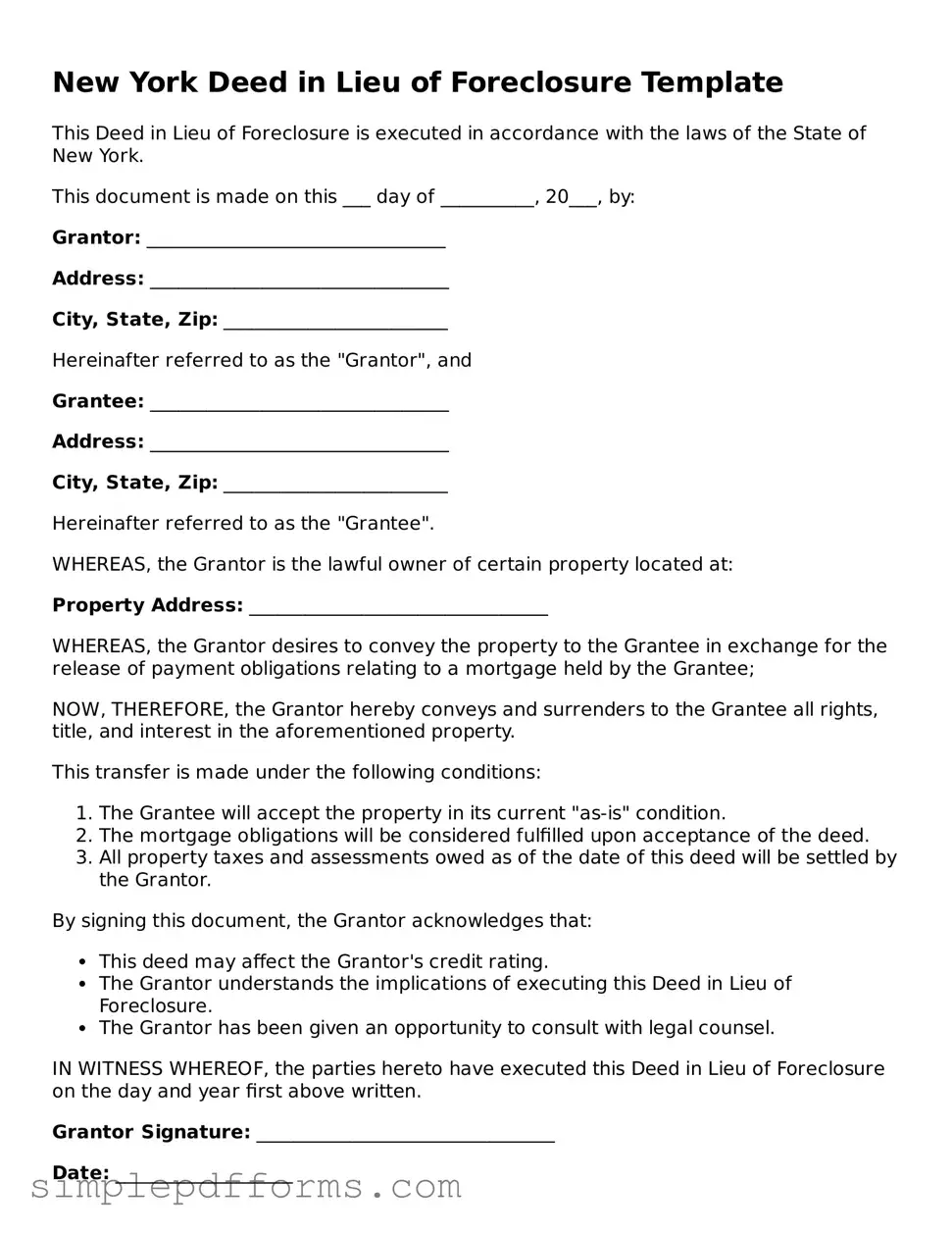

New York Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is executed in accordance with the laws of the State of New York.

This document is made on this ___ day of __________, 20___, by:

Grantor: ________________________________

Address: ________________________________

City, State, Zip: ________________________

Hereinafter referred to as the "Grantor", and

Grantee: ________________________________

Address: ________________________________

City, State, Zip: ________________________

Hereinafter referred to as the "Grantee".

WHEREAS, the Grantor is the lawful owner of certain property located at:

Property Address: ________________________________

WHEREAS, the Grantor desires to convey the property to the Grantee in exchange for the release of payment obligations relating to a mortgage held by the Grantee;

NOW, THEREFORE, the Grantor hereby conveys and surrenders to the Grantee all rights, title, and interest in the aforementioned property.

This transfer is made under the following conditions:

By signing this document, the Grantor acknowledges that:

IN WITNESS WHEREOF, the parties hereto have executed this Deed in Lieu of Foreclosure on the day and year first above written.

Grantor Signature: ________________________________

Date: ___________________

Grantee Signature: ________________________________

Date: ___________________

STATE OF NEW YORK

COUNTY OF __________________

On this ___ day of __________, 20___, before me personally appeared __________________, known to me to be the person described herein and who executed the within instrument, and acknowledged that he/she executed the same.

Notary Public Signature: ________________________________

Commission Expires: ________________________________