Fill a Valid Mortgage Statement Form

Simple PDF Forms

Fill a Valid Mortgage Statement Form

Understanding your mortgage statement can be confusing, and there are several misconceptions that people often have about it. Here are seven common myths, along with clarifications to help you better understand your mortgage statement.

This is not true. The mortgage statement is primarily for you, the borrower. It provides essential information about your loan, payment history, and any fees that may apply.

While late fees can be charged if payments are not received by the due date, they are not applied unless you miss a payment. Your statement will indicate when a late fee is applicable.

Escrow payments, which cover property taxes and insurance, are often required by lenders. They help ensure that these important expenses are paid on time, protecting both you and the lender.

Partial payments do not apply to your mortgage balance. Instead, they are held in a suspense account until the full payment is made. This can lead to additional fees and complications.

This is a common concern, but it’s important to remember that processing times can vary. Always keep your payment confirmation and contact your servicer if you have questions.

Not all mortgages have fixed interest rates. Some loans may have adjustable rates that change after a certain period. Your statement will indicate the type of interest rate you have.

This is a risky approach. Ignoring a delinquency notice can lead to serious consequences, including additional fees and potential foreclosure. It’s crucial to address any overdue payments as soon as possible.

Completing the Mortgage Statement form requires careful attention to detail. This document is essential for managing your mortgage account and understanding your payment obligations. Follow the steps below to ensure that you fill out the form accurately.

Completing a Mortgage Statement form requires attention to detail. One common mistake is failing to include the correct account number. This number is crucial for the servicer to identify your loan. Without it, payments may not be applied correctly, leading to potential late fees or other issues.

Another frequent error is neglecting to update the payment due date. If this date is incorrect, it can create confusion about when payments are expected. This oversight can result in missed payments and additional fees, which can complicate your financial situation.

Many individuals also overlook the interest rate section. Entering an outdated or incorrect interest rate can mislead both the borrower and the servicer. This mistake can affect calculations related to the total amount due and future payment obligations.

Additionally, failing to specify whether there is a prepayment penalty can lead to unexpected charges. If a borrower plans to pay off the mortgage early, understanding whether a penalty exists is essential. Omitting this information can result in financial surprises down the line.

Another common mistake is not accurately detailing the transaction activity. This section provides a history of payments and charges. Inaccuracies here can lead to disputes over payment status and outstanding balances, creating unnecessary stress for the borrower.

Lastly, many people forget to include the total amount enclosed when submitting the form. This can delay processing and may result in additional fees if the payment is not received on time. Ensuring that all required information is complete and accurate is vital for a smooth mortgage management process.

| Fact Name | Description |

|---|---|

| Servicer Information | The mortgage statement includes the name of the servicer, their customer service phone number, and website. |

| Statement Date | The statement date indicates when the mortgage statement was generated. |

| Payment Due Date | This date specifies when the next mortgage payment is due. |

| Late Fee Policy | If payment is received after the specified date, a late fee will be charged. |

| Outstanding Principal | The statement shows the remaining principal balance on the mortgage. |

| Prepayment Penalty | The form indicates whether there is a prepayment penalty for paying off the mortgage early. |

| Delinquency Notice | A notice is included if the borrower is late on payments, warning of potential fees and foreclosure. |

A Mortgage Statement is a document provided by your loan servicer that details your mortgage account information. It includes your outstanding balance, payment history, and any fees that may apply. This statement helps you understand your financial obligations related to your mortgage.

Your Mortgage Statement contains several key pieces of information:

If you miss a payment, a late fee will be charged as indicated on your statement. Additionally, your account may become delinquent, which could lead to further fees and potential foreclosure. It is crucial to address missed payments promptly to avoid these consequences.

Partial payments are amounts less than your total monthly payment. These payments are not applied directly to your mortgage balance but are held in a separate suspense account. To apply a partial payment to your mortgage, you must pay the remaining balance of that payment.

If you are facing financial challenges, it is important to seek assistance. Your Mortgage Statement may provide information on mortgage counseling or assistance programs. Contact your loan servicer for guidance tailored to your situation.

You can make a payment by mailing a check payable to your loan servicer, as indicated on your Mortgage Statement. Ensure you include your account number on the check to avoid processing delays. Some servicers also offer online payment options through their website.

Your Mortgage Statement includes customer service contact information for your loan servicer. You can reach them by phone or visit their website for additional support. Don't hesitate to ask questions regarding your account or payments.

When managing a mortgage, several documents often accompany the Mortgage Statement form. Each serves a distinct purpose, providing essential information to both the borrower and the lender. Understanding these documents can help borrowers navigate their financial responsibilities more effectively.

By familiarizing themselves with these documents, borrowers can maintain better control over their mortgage and avoid potential pitfalls. Each document plays a vital role in the overall management of a mortgage, contributing to a clearer understanding of one’s financial situation.

Dispute Documents@netspend - A timely submission is essential for resolving your dispute effectively.

Using the proper documentation is essential when engaging in any vehicle sale, particularly with RVs, where clarity is crucial. The South Carolina RV Bill of Sale form acts as a safeguard for both parties, ensuring all necessary transaction details are properly recorded. For further assistance, you can access the Vehicle Bill of Sale Forms which can provide a helpful guide during the process.

Employer's Quarterly Federal Tax Return - Form 941 allows employers to claim any refundable tax credits.

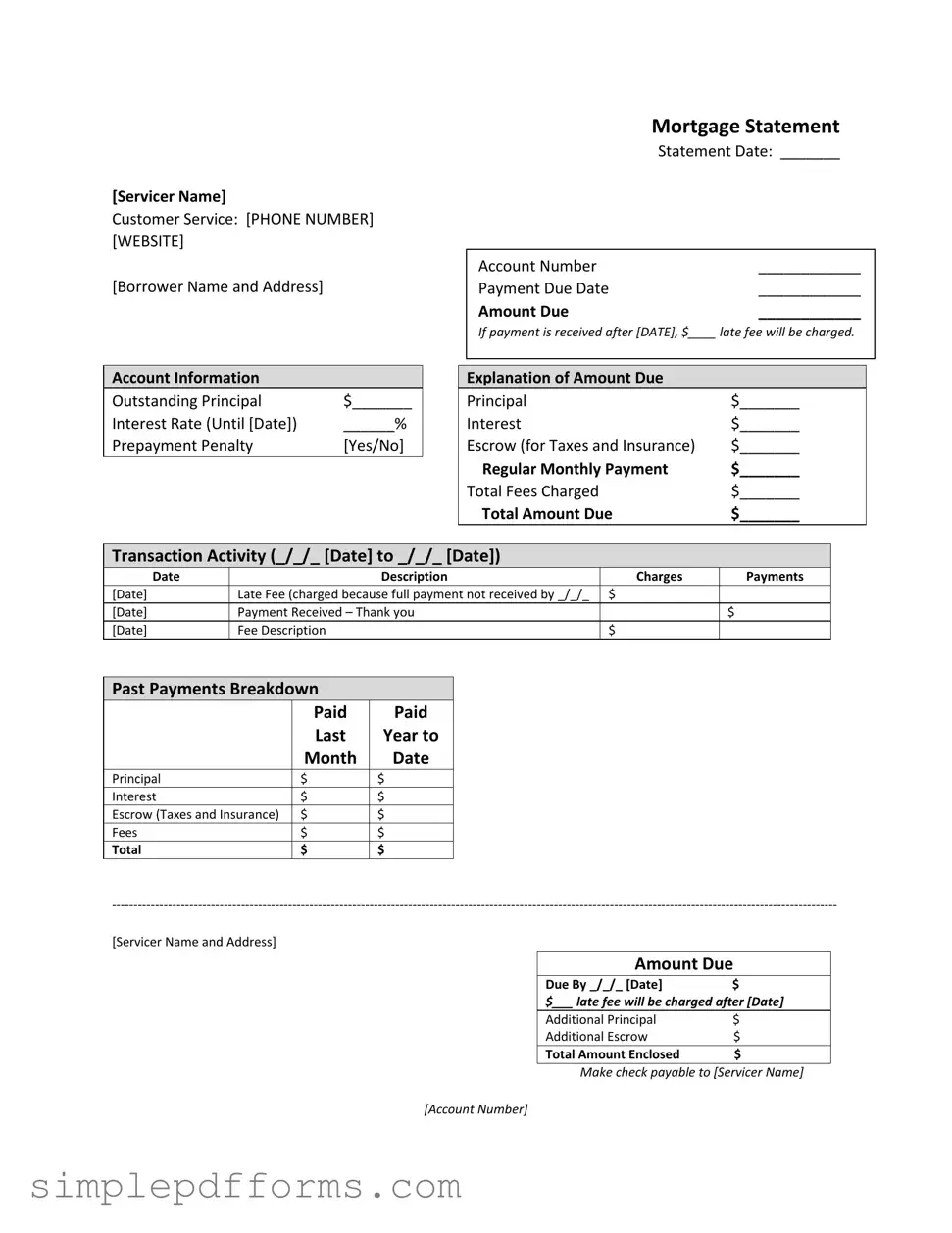

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.