Free Loan Agreement Form

Simple PDF Forms

Free Loan Agreement Form

Loan agreements are often misunderstood documents. Many people have misconceptions about their purpose and function. Here are seven common misconceptions:

Many believe that all loan agreements follow a standard template. In reality, each agreement is tailored to the specific terms negotiated between the lender and borrower.

Some borrowers think they can sign without reading. This is a risky assumption. Understanding the terms is crucial to avoid unpleasant surprises later.

People often think that small loans can be informal. However, even small loans can benefit from a written agreement to clarify terms and protect both parties.

Many believe that only banks use loan agreements. In fact, any lender, including individuals and businesses, can create a loan agreement.

Some assume that loan agreements are set in stone. However, parties can negotiate changes if both agree, often through an amendment.

While repayment terms are important, loan agreements also cover interest rates, collateral, and default conditions. Understanding all these elements is essential.

Not every agreement holds legal weight. For a loan agreement to be enforceable, it must meet certain legal requirements, including being in writing and signed by both parties.

Completing the Loan Agreement form is a crucial step in securing the necessary funding for your needs. It is important to approach this process with care and attention to detail. Following the steps outlined below will help ensure that your form is filled out accurately and completely.

After completing these steps, you will be ready to submit the Loan Agreement form. It is advisable to keep a copy for your records and to follow up with the lender if you do not receive a timely response.

Filling out a Loan Agreement form can seem straightforward, but many people make common mistakes that can lead to complications down the road. One frequent error is not providing accurate personal information. When individuals rush through the form, they may accidentally misspell their names or provide incorrect addresses. These small mistakes can create significant issues later, especially when it comes to verifying identity or sending important documents.

Another common mistake is failing to read the terms and conditions thoroughly. Many borrowers skim over the fine print, which often contains crucial information about interest rates, repayment schedules, and penalties for late payments. Understanding these terms is essential to avoid surprises later on. It’s always best to take the time to read and comprehend what you are agreeing to.

Some individuals overlook the importance of providing complete financial information. Lenders need a clear picture of your financial situation to assess your eligibility for the loan. If you leave out details about your income, expenses, or existing debts, it may lead to delays in processing your application or even denial of the loan.

Another mistake is not being honest about your financial situation. Some borrowers might inflate their income or downplay their debts in hopes of securing a better loan. This approach can backfire. If a lender discovers discrepancies, it could result in losing trust and possibly facing legal consequences.

In addition, many people fail to check for errors after completing the form. Typos or incorrect figures can easily slip through the cracks. Before submitting, it’s wise to review the entire document carefully. A second pair of eyes can also help catch mistakes that you might have missed.

Not asking questions is another pitfall. If something is unclear, borrowers may hesitate to seek clarification. This can lead to misunderstandings about the loan terms. It’s important to communicate with the lender about any uncertainties to ensure you fully understand your obligations.

Another mistake is ignoring the importance of having a co-signer when necessary. If your credit history isn’t strong, having a co-signer can improve your chances of approval. Some borrowers may not realize this option is available to them and miss out on better loan terms.

Lastly, many people underestimate the significance of keeping a copy of the completed Loan Agreement. Once the form is submitted, it’s crucial to retain a copy for your records. This will help you reference the terms later and ensure that both parties are on the same page.

| Fact Name | Description |

|---|---|

| Definition | A Loan Agreement is a legal document outlining the terms and conditions of a loan between a lender and a borrower. |

| Parties Involved | The agreement typically involves two parties: the lender, who provides the funds, and the borrower, who receives the funds. |

| Governing Law | The governing law for Loan Agreements varies by state. For example, California law applies to agreements executed in California. |

| Key Terms | Essential terms include the loan amount, interest rate, repayment schedule, and consequences of default. |

| Security Interest | In some cases, the lender may require collateral to secure the loan, which is specified in the agreement. |

| Amendments | Any changes to the Loan Agreement must be documented in writing and signed by both parties to be enforceable. |

What is a Loan Agreement?

A Loan Agreement is a formal document that outlines the terms and conditions under which one party lends money to another. It specifies the loan amount, interest rate, repayment schedule, and any collateral involved. This document serves to protect both the lender and the borrower by clearly defining their rights and responsibilities.

Who should use a Loan Agreement?

Any individual or entity involved in a lending transaction should consider using a Loan Agreement. This includes personal loans between friends or family, business loans, and formal lending institutions. Having a written agreement helps ensure clarity and reduces the potential for disputes.

What are the key components of a Loan Agreement?

How is interest calculated in a Loan Agreement?

Interest can be calculated in several ways, typically either as simple interest or compound interest. Simple interest is calculated on the principal amount only, while compound interest is calculated on the principal plus any accrued interest. The Loan Agreement should clearly state the method used for calculating interest to avoid confusion.

Can a Loan Agreement be modified?

Yes, a Loan Agreement can be modified if both parties agree to the changes. It is important to document any modifications in writing and have both parties sign the amended agreement. This ensures that all parties are aware of and agree to the new terms.

What happens if the borrower defaults on the loan?

If the borrower defaults, the lender has the right to take specific actions as outlined in the Loan Agreement. This may include demanding immediate repayment of the outstanding balance, taking possession of collateral, or pursuing legal action. The specific consequences of default should be clearly stated in the agreement.

Is it necessary to have a lawyer review a Loan Agreement?

While it is not strictly necessary, having a lawyer review a Loan Agreement can be beneficial. A legal professional can ensure that the agreement complies with state laws and adequately protects your interests. This is especially important for larger loans or complex agreements.

How can I ensure the Loan Agreement is enforceable?

To ensure enforceability, the Loan Agreement should be clear, detailed, and signed by both parties. It should comply with local laws and regulations. Additionally, both parties should keep copies of the signed agreement for their records. This helps establish the agreement's validity in case of disputes.

When entering into a loan agreement, several other forms and documents may accompany it to ensure clarity and protection for all parties involved. These documents help outline the terms of the loan, provide necessary disclosures, and establish the rights and responsibilities of each party. Below is a list of commonly used documents that often accompany a Loan Agreement.

Understanding these documents is essential for anyone involved in a loan transaction. Each plays a crucial role in safeguarding the interests of both the lender and the borrower, helping to create a clear and transparent lending process.

Cdph Tb Risk Assessment - The lot number of the PPD solution used for the test is required on the form.

Fl-680 - In the case of incomplete immunizations, the form provides a way to document ongoing schedules for required doses.

Texas Temporary Tag - Essential for new vehicle owners awaiting permanent tags.

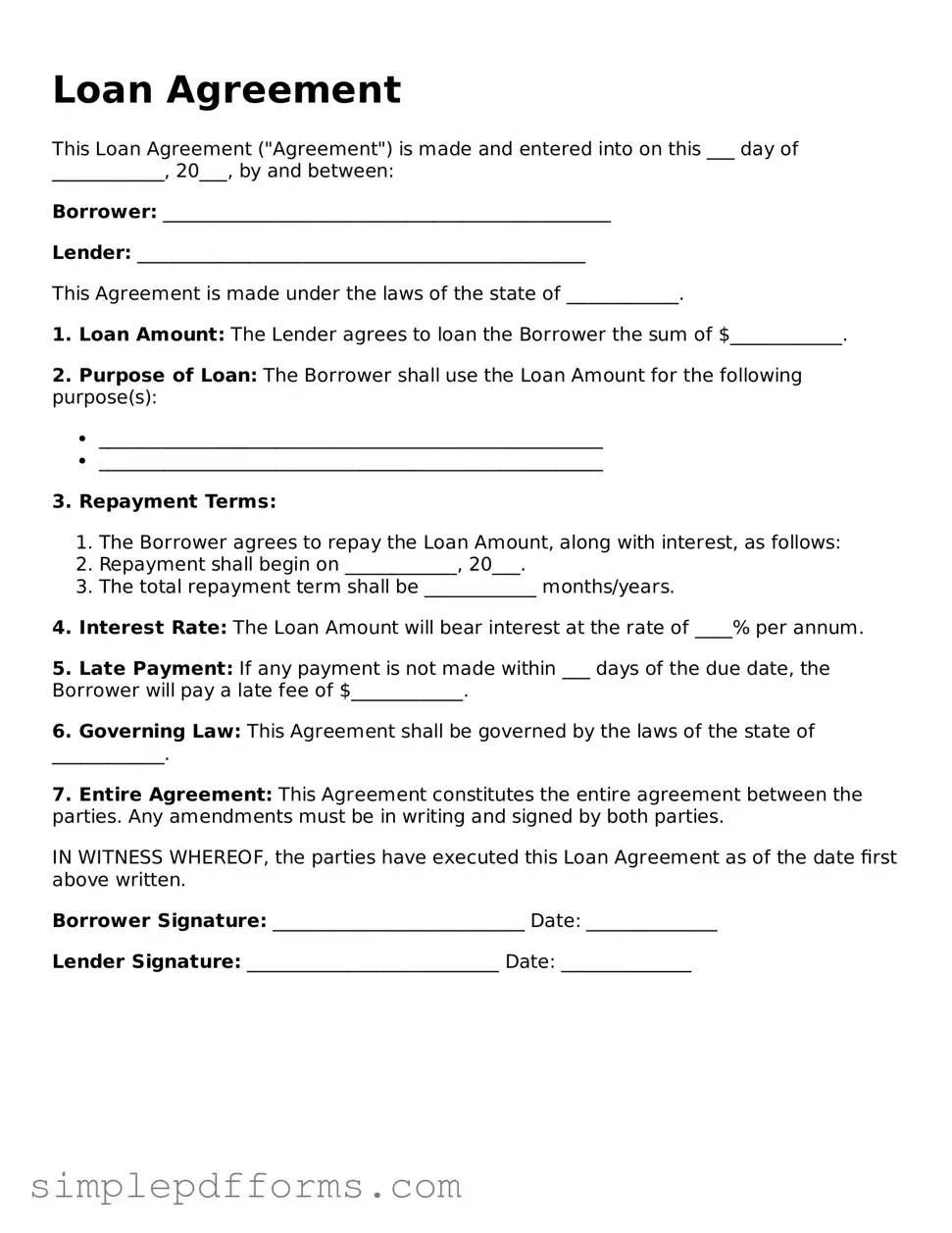

Loan Agreement

This Loan Agreement ("Agreement") is made and entered into on this ___ day of ____________, 20___, by and between:

Borrower: ________________________________________________

Lender: ________________________________________________

This Agreement is made under the laws of the state of ____________.

1. Loan Amount: The Lender agrees to loan the Borrower the sum of $____________.

2. Purpose of Loan: The Borrower shall use the Loan Amount for the following purpose(s):

3. Repayment Terms:

4. Interest Rate: The Loan Amount will bear interest at the rate of ____% per annum.

5. Late Payment: If any payment is not made within ___ days of the due date, the Borrower will pay a late fee of $____________.

6. Governing Law: This Agreement shall be governed by the laws of the state of ____________.

7. Entire Agreement: This Agreement constitutes the entire agreement between the parties. Any amendments must be in writing and signed by both parties.

IN WITNESS WHEREOF, the parties have executed this Loan Agreement as of the date first above written.

Borrower Signature: ___________________________ Date: ______________

Lender Signature: ___________________________ Date: ______________