Attorney-Verified Deed in Lieu of Foreclosure Document for Illinois State

Simple PDF Forms

Attorney-Verified Deed in Lieu of Foreclosure Document for Illinois State

Understanding the Illinois Deed in Lieu of Foreclosure form is essential for homeowners facing financial difficulties. Unfortunately, several misconceptions can cloud judgment and lead to poor decision-making. Here are eight common misconceptions explained:

Being informed about these misconceptions can help homeowners make better decisions regarding their financial futures. Understanding the implications of a deed in lieu of foreclosure is crucial in navigating this challenging situation.

Once you have the Illinois Deed in Lieu of Foreclosure form, it’s important to fill it out accurately. This document will need to be signed and notarized before submission. Follow these steps carefully to ensure everything is completed correctly.

After filling out the form and submitting it, you will want to keep track of any correspondence from the lender. Ensure that you receive confirmation of the deed's acceptance and any further instructions regarding your situation.

Filling out the Illinois Deed in Lieu of Foreclosure form can be a complex process, and mistakes can lead to significant delays or complications. One common error is failing to provide accurate property information. It’s essential to ensure that the property address and legal description are correct. Inaccuracies can create confusion and may result in the deed being deemed invalid.

Another frequent mistake is not properly identifying the parties involved. Both the borrower and the lender must be clearly named in the document. Omitting names or using incorrect spellings can complicate the transfer of ownership. It's crucial to double-check all names against official records to avoid this issue.

Many individuals overlook the need for signatures. The form requires the borrower’s signature, and in some cases, the lender’s representative may also need to sign. Neglecting to sign the document can render it ineffective. Always ensure that all necessary parties have signed before submitting the form.

Additionally, people sometimes fail to include a notary acknowledgment. In Illinois, the deed must be notarized to be legally binding. Skipping this step can lead to problems with the acceptance of the deed. It’s advisable to have a notary present when signing the document to ensure compliance with this requirement.

Some individuals may also misinterpret the implications of the deed. A Deed in Lieu of Foreclosure is not just a simple transfer of property; it can have significant consequences for credit ratings and future borrowing. Understanding these implications is vital before proceeding with the form.

Lastly, neglecting to consult with a professional can be a costly mistake. Many people attempt to fill out the form without seeking legal or financial advice. This can lead to errors that could have been easily avoided. Engaging with a knowledgeable professional can provide clarity and ensure that the form is completed correctly.

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal document where a borrower voluntarily transfers ownership of their property to the lender to avoid foreclosure proceedings. |

| Governing Law | The process is governed by Illinois law, specifically under the Illinois Mortgage Foreclosure Law (IMFL). |

| Eligibility | Homeowners facing financial hardship may qualify for a deed in lieu of foreclosure, provided they have exhausted other options such as loan modification. |

| Advantages | This option can help borrowers avoid the lengthy and costly foreclosure process, and it may have a less severe impact on their credit score. |

| Documentation Required | Typically, borrowers must provide financial statements, proof of hardship, and any other documentation requested by the lender. |

| Release of Liability | In many cases, lenders may agree to release the borrower from any further liability on the mortgage after the deed is executed. |

| Potential Drawbacks | Borrowers should be aware that while a deed in lieu may mitigate some consequences, it can still affect their credit and may have tax implications. |

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal process where a homeowner voluntarily transfers the title of their property to the lender to avoid foreclosure. This can be a beneficial option for those who are struggling to make mortgage payments and want to prevent the negative consequences of foreclosure on their credit report.

How does a Deed in Lieu of Foreclosure work?

In this process, the homeowner contacts their lender to discuss the possibility of a Deed in Lieu. If both parties agree, the homeowner signs the deed, transferring ownership of the property to the lender. In exchange, the lender typically forgives the remaining mortgage debt, allowing the homeowner to walk away without further financial obligation.

What are the benefits of choosing a Deed in Lieu of Foreclosure?

Are there any drawbacks to a Deed in Lieu of Foreclosure?

While there are benefits, there are also potential drawbacks. The homeowner may still face tax implications if the lender forgives a portion of the debt. Additionally, not all lenders accept Deeds in Lieu, and some may require the homeowner to prove financial hardship. It is essential to consider these factors before proceeding.

What are the eligibility requirements for a Deed in Lieu of Foreclosure?

Eligibility can vary by lender, but generally, homeowners must demonstrate financial hardship and be unable to keep up with mortgage payments. Lenders may also require that the property be in good condition and that the homeowner has not filed for bankruptcy recently. Each situation is unique, so it is crucial to communicate openly with the lender.

What happens to the homeowner after the Deed in Lieu is completed?

Once the Deed in Lieu is executed, the homeowner will no longer own the property and should receive confirmation from the lender regarding the forgiveness of the remaining debt. Homeowners may need to find new housing and may want to consult a financial advisor to understand the implications for their future financial situation.

Can a Deed in Lieu of Foreclosure affect my credit score?

Yes, a Deed in Lieu of Foreclosure can impact your credit score, but typically less severely than a foreclosure. The exact effect will depend on various factors, including your overall credit history and the policies of credit reporting agencies. However, it is generally viewed more favorably than a foreclosure.

How can I start the process of a Deed in Lieu of Foreclosure?

The first step is to contact your lender. Discuss your financial situation and express your interest in pursuing a Deed in Lieu of Foreclosure. Be prepared to provide documentation of your financial hardship. It may also be beneficial to seek advice from a housing counselor or attorney who specializes in foreclosure alternatives to guide you through the process.

In the context of real estate transactions, particularly those involving distressed properties, a Deed in Lieu of Foreclosure serves as a mechanism to transfer ownership from the borrower to the lender. However, several other documents often accompany this form to ensure a comprehensive understanding of the transaction and to protect the interests of all parties involved. Below is a list of these essential documents.

Each of these documents plays a critical role in the process surrounding a Deed in Lieu of Foreclosure. They help clarify the rights and responsibilities of the parties involved, facilitate a smoother transition of ownership, and mitigate potential legal complications. Understanding these documents can empower individuals navigating the complexities of real estate transactions, especially in challenging financial situations.

Foreclosure Vs Deed in Lieu - Homeowners should consider the impact on their future housing options prior to signing a Deed in Lieu.

Deed in Lieu of Foreclosure Sample - This document helps facilitate the return of the property to the financial institution.

Foreclosure Deed - Borrowers should understand their rights and responsibilities when considering a Deed in Lieu of Foreclosure.

To obtain the necessary documentation for transferring a trailer's ownership, you can visit the following link for the Trailer Bill of Sale: https://mypdfform.com/blank-arizona-trailer-bill-of-sale/, which provides a straightforward template to ensure all required details are included in the sale process.

Will I Owe Money After a Deed in Lieu of Foreclosure - Exploring all alternatives, including loan modifications or short sales, is essential before opting for a Deed in Lieu.

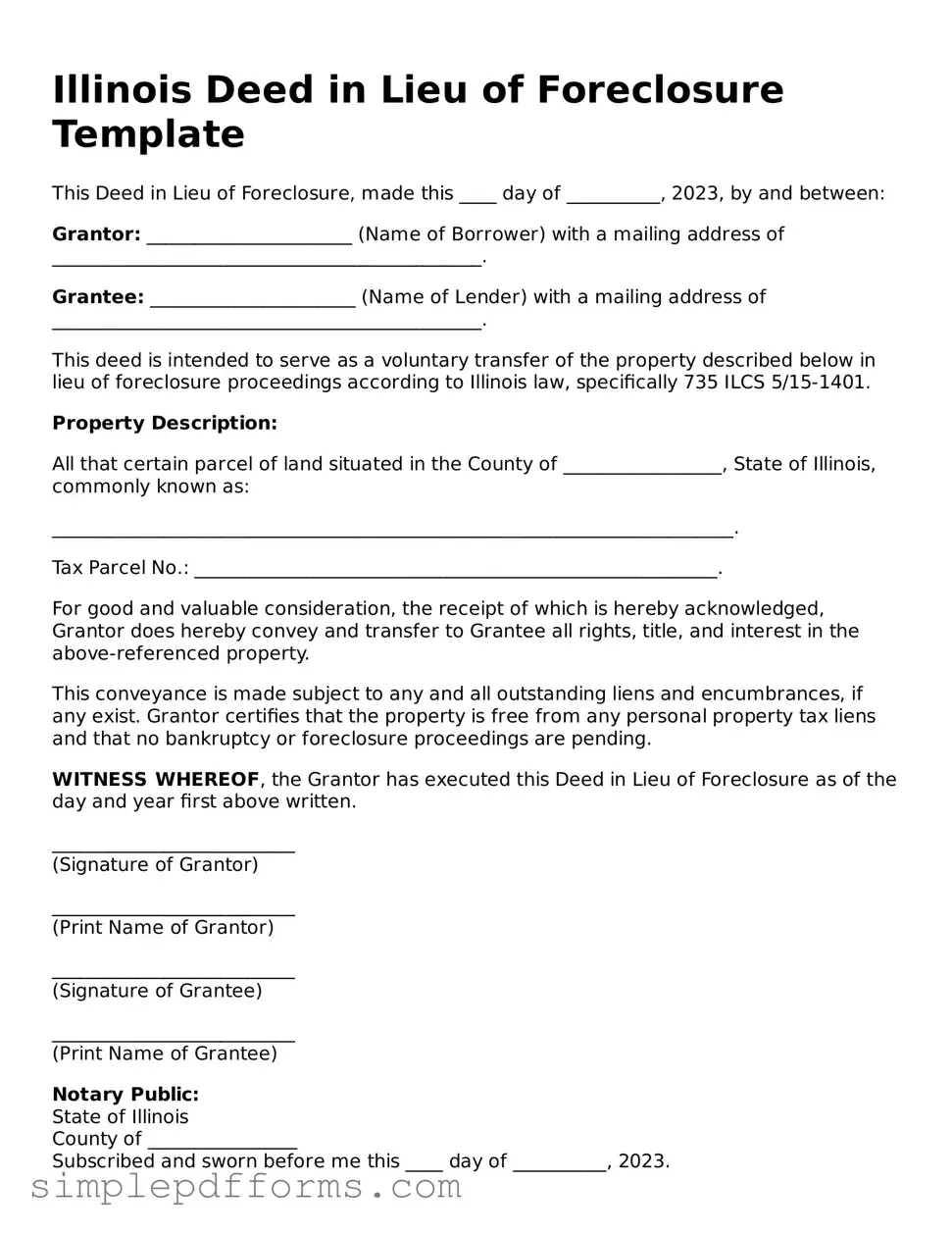

Illinois Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure, made this ____ day of __________, 2023, by and between:

Grantor: ______________________ (Name of Borrower) with a mailing address of ______________________________________________.

Grantee: ______________________ (Name of Lender) with a mailing address of ______________________________________________.

This deed is intended to serve as a voluntary transfer of the property described below in lieu of foreclosure proceedings according to Illinois law, specifically 735 ILCS 5/15-1401.

Property Description:

All that certain parcel of land situated in the County of _________________, State of Illinois, commonly known as:

_________________________________________________________________________.

Tax Parcel No.: ________________________________________________________.

For good and valuable consideration, the receipt of which is hereby acknowledged, Grantor does hereby convey and transfer to Grantee all rights, title, and interest in the above-referenced property.

This conveyance is made subject to any and all outstanding liens and encumbrances, if any exist. Grantor certifies that the property is free from any personal property tax liens and that no bankruptcy or foreclosure proceedings are pending.

WITNESS WHEREOF, the Grantor has executed this Deed in Lieu of Foreclosure as of the day and year first above written.

__________________________

(Signature of Grantor)

__________________________

(Print Name of Grantor)

__________________________

(Signature of Grantee)

__________________________

(Print Name of Grantee)

Notary Public:

State of Illinois

County of ________________

Subscribed and sworn before me this ____ day of __________, 2023.

__________________________

Signature of Notary Public

My Commission Expires: ____________________