Free Employee Loan Agreement Form

Simple PDF Forms

Free Employee Loan Agreement Form

Misconceptions about the Employee Loan Agreement form can lead to confusion and mismanagement. Here are four common misunderstandings:

Many believe that the Employee Loan Agreement is a one-size-fits-all document. In reality, each agreement should be tailored to fit the specific circumstances of the loan, including the amount, interest rate, and repayment terms.

This form is often thought to be necessary only for large organizations. However, any employer, regardless of size, can benefit from having a clear agreement in place to protect both the employer and the employee.

Some people think that a verbal agreement is enough to secure a loan. This is misleading. A written agreement provides legal protection and clarity, reducing the risk of misunderstandings later on.

There is a belief that the terms of the agreement are set in stone once signed. In fact, amendments can be made if both parties agree, ensuring the terms remain relevant and fair over time.

Filling out the Employee Loan Agreement form is a straightforward process that ensures both the employee and employer are clear on the terms of the loan. Follow these steps carefully to complete the form accurately.

Once the form is submitted, it will be reviewed, and the employee will be notified of the next steps regarding the loan approval process.

Filling out an Employee Loan Agreement form is a critical step for both employees and employers. However, mistakes can easily occur during this process. Understanding common pitfalls can help ensure that the agreement is completed accurately and effectively.

One frequent mistake is failing to provide accurate personal information. Employees may overlook details such as their full legal name, address, or social security number. This information is essential for identification and record-keeping purposes. Missing or incorrect details can lead to complications down the line.

Another common error is not specifying the loan amount clearly. Employees sometimes write ambiguous figures or forget to include decimals. A precise loan amount is crucial for both parties to understand the financial obligation involved. Miscommunication about the amount can lead to disputes later.

Many individuals also neglect to outline the repayment terms. This includes the interest rate, payment schedule, and duration of the loan. Without clear terms, misunderstandings may arise regarding when payments are due and how much is owed. Clarity in this area protects both the employee and employer.

Some employees fail to read the entire agreement before signing. This oversight can lead to unintentional acceptance of terms that may not be favorable. Taking the time to review the document ensures that all parties are aware of their rights and responsibilities.

In addition, individuals often forget to include signatures where required. Both the employee and employer must sign the agreement for it to be legally binding. Missing signatures can render the document invalid, leading to potential issues with enforcement.

Another mistake involves not keeping a copy of the signed agreement. Employees may assume that the employer will retain a copy, but having one for personal records is essential. This ensures that both parties can refer back to the terms of the loan if necessary.

People sometimes misinterpret the implications of defaulting on the loan. It is vital to understand what happens if payments are missed. Clarity about consequences can help employees make informed decisions about their financial commitments.

Lastly, some individuals overlook the importance of discussing the loan with their employer before filling out the form. Open communication can clarify expectations and help address any concerns. A collaborative approach fosters a better understanding of the agreement.

By being aware of these common mistakes, employees can fill out the Employee Loan Agreement form with greater confidence. Taking care to avoid these pitfalls helps ensure a smooth and transparent process for both parties involved.

| Fact Name | Description |

|---|---|

| Definition | An Employee Loan Agreement is a formal document outlining the terms under which an employer lends money to an employee. |

| Purpose | This agreement serves to protect both parties by clearly stating the loan amount, repayment terms, and any applicable interest rates. |

| Repayment Terms | Typically, the agreement specifies how and when the employee must repay the loan, which can include payroll deductions. |

| State-Specific Laws | Each state may have different regulations governing employee loans. For example, California law requires specific disclosures to be made in the agreement. |

| Interest Rates | Interest rates on employee loans may be lower than those offered by traditional lenders, but must comply with state usury laws. |

| Confidentiality | Employee Loan Agreements often include confidentiality clauses to protect the financial information of the employee. |

What is an Employee Loan Agreement?

An Employee Loan Agreement is a document that outlines the terms and conditions under which an employer provides a loan to an employee. It details the amount of the loan, repayment schedule, interest rates, and any other relevant terms.

Who should use this agreement?

This agreement is ideal for employers who want to offer financial assistance to their employees. It is also useful for employees who need to borrow money from their employer in a structured and formal manner.

What details are included in the agreement?

Is there a limit to how much I can loan an employee?

There is no set limit for employee loans, but employers should consider the employee's ability to repay the loan. It's also wise to check for any company policies regarding loan amounts.

What happens if the employee cannot repay the loan?

The agreement should clearly outline the consequences of default. This may include deductions from the employee's paycheck, legal action, or other measures as agreed upon in the contract.

Are there tax implications for the employer?

Yes, there can be tax implications. Employers should consult with a tax professional to understand how providing a loan may affect their tax obligations and the employee's tax situation.

Can the loan be forgiven?

If the employer wishes to forgive the loan, this should be documented in writing. Forgiveness may have tax implications for both parties, so it’s important to seek advice from a tax professional.

Is it necessary to have a written agreement?

Yes, having a written agreement is crucial. It provides clarity and protection for both the employer and the employee. A verbal agreement may lead to misunderstandings and disputes.

Can this agreement be modified?

Yes, the agreement can be modified if both parties agree to the changes. Any modifications should be documented in writing and signed by both the employer and the employee.

Where can I find a template for an Employee Loan Agreement?

Templates for Employee Loan Agreements can often be found online through legal form websites or business resources. It’s advisable to customize any template to fit your specific situation and consult a legal professional if needed.

An Employee Loan Agreement form is a crucial document that outlines the terms and conditions of a loan provided by an employer to an employee. To ensure clarity and legal compliance, several other forms and documents are often used in conjunction with this agreement. Below is a list of these documents, each serving a specific purpose.

Using these documents in conjunction with the Employee Loan Agreement helps protect both the employer and employee. Clarity in the loan process fosters a positive working relationship and reduces the potential for misunderstandings.

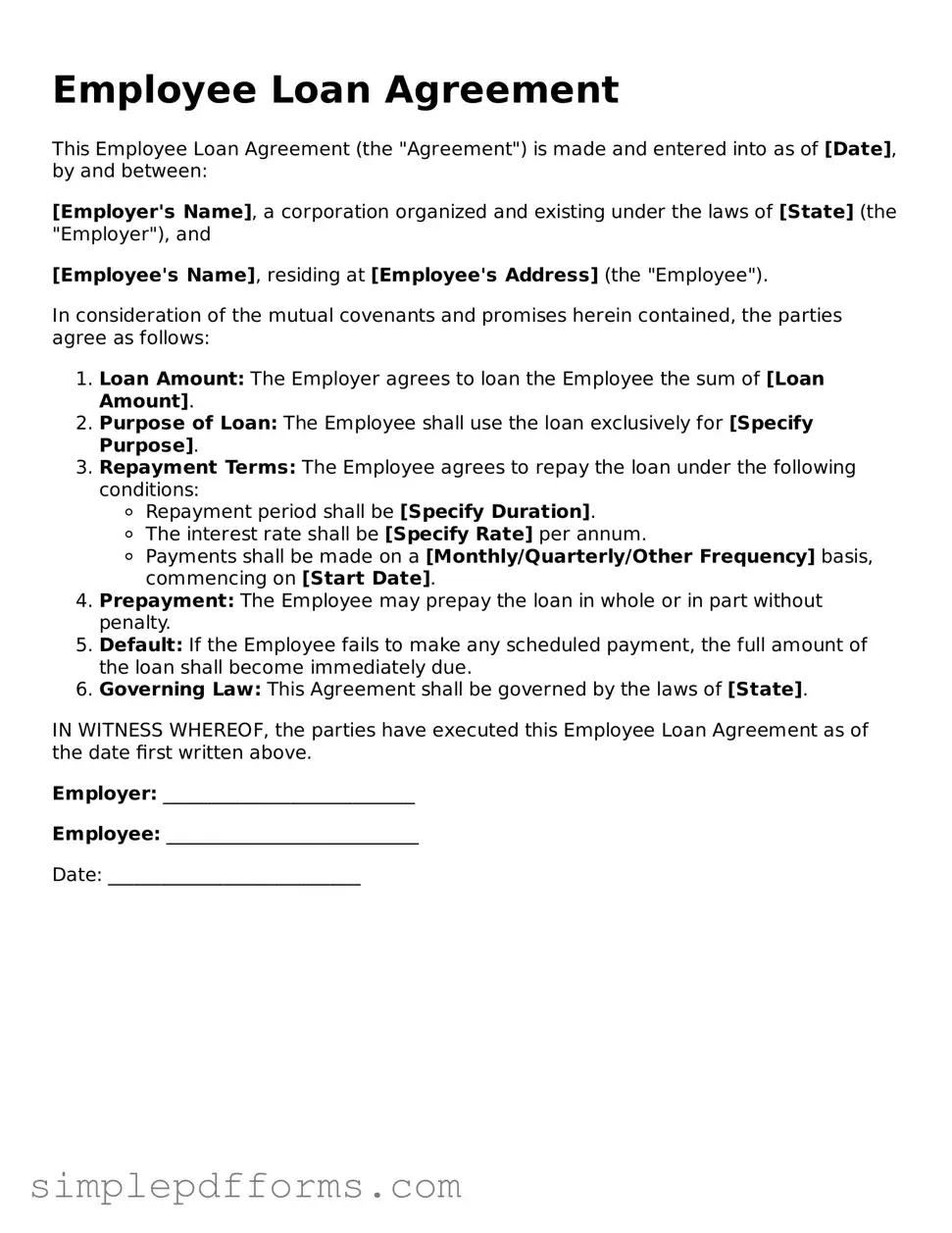

Employee Loan Agreement

This Employee Loan Agreement (the "Agreement") is made and entered into as of [Date], by and between:

[Employer's Name], a corporation organized and existing under the laws of [State] (the "Employer"), and

[Employee's Name], residing at [Employee's Address] (the "Employee").

In consideration of the mutual covenants and promises herein contained, the parties agree as follows:

IN WITNESS WHEREOF, the parties have executed this Employee Loan Agreement as of the date first written above.

Employer: ___________________________

Employee: ___________________________

Date: ___________________________