Fill a Valid Cg 20 10 07 04 Liability Endorsement Form

Simple PDF Forms

Fill a Valid Cg 20 10 07 04 Liability Endorsement Form

Understanding the Cg 20 10 07 04 Liability Endorsement form can be challenging. Here are seven common misconceptions that often arise:

By clarifying these misconceptions, stakeholders can better understand the scope and limitations of the Cg 20 10 07 04 Liability Endorsement form, ensuring they make informed decisions regarding their insurance needs.

Completing the CG 20 10 07 04 Liability Endorsement form requires careful attention to detail. This form is essential for adding additional insured parties to a general liability policy. Follow these steps to ensure accurate completion.

Once the form is completed, it should be submitted to your insurance provider for processing. Ensure that you keep a copy for your records, as it may be needed for future reference or claims.

When filling out the CG 20 10 07 04 Liability Endorsement form, many people make critical mistakes that can lead to complications down the line. One common error is failing to clearly list the additional insured person(s) or organization(s) in the designated section. This omission can result in a lack of coverage, leaving parties exposed to potential liability.

Another mistake is not providing the correct location(s) of covered operations. If the locations are inaccurate or incomplete, it can create confusion regarding where the coverage applies. This could lead to disputes over claims and ultimately impact the effectiveness of the insurance.

Many individuals also overlook the importance of understanding the implications of the endorsement. They may not realize that the coverage for additional insureds is limited to specific situations. If the form is completed without this understanding, it could lead to unexpected gaps in coverage.

In addition, some people neglect to read the fine print regarding exclusions. The form states that coverage does not apply after certain conditions are met, such as when all work has been completed. Ignoring these exclusions can lead to significant financial repercussions if a claim arises after the work is done.

Another frequent mistake is misunderstanding the limits of insurance. Many individuals fail to recognize that the endorsement will not increase the applicable limits of insurance. If the amount required by a contract is less than the available limits, this can create confusion during claims processing.

Additionally, some may not provide accurate information regarding their acts or omissions. This section is crucial, as it defines the circumstances under which the additional insured is covered. Inaccurate descriptions can lead to denied claims and disputes over liability.

People also often forget to update the form when changes occur. If there are modifications to the additional insureds or the locations of operations, these should be reflected on the form. Neglecting to make these updates can result in outdated information that undermines the policy's effectiveness.

Lastly, not consulting with an insurance professional can lead to incomplete or incorrect submissions. Many individuals assume they understand the requirements fully, but having expert guidance can help avoid pitfalls. It’s always wise to seek assistance to ensure the form is filled out accurately and comprehensively.

| Fact Name | Details |

|---|---|

| Policy Number | CG 20 10 12 19 |

| Purpose | This endorsement adds additional insured coverage for owners, lessees, or contractors. |

| Coverage Type | Covers liability for bodily injury, property damage, or personal and advertising injury. |

| Conditions for Coverage | Coverage applies only for acts or omissions in the performance of ongoing operations for the additional insured. |

| Exclusions | Does not cover injuries or damages occurring after work has been completed or the project has been put to intended use. |

| Limits of Insurance | The maximum payment is the lesser of the contract-required amount or the available insurance limits. |

| Governing Law | Varies by state; typically governed by state insurance regulations. |

| Importance of Reading | Policyholders should read the endorsement carefully to understand its implications and limitations. |

This endorsement is designed to add specific individuals or organizations as additional insureds under a Commercial General Liability policy. It provides coverage for liabilities arising from bodily injury, property damage, or personal and advertising injury that occur during ongoing operations for the additional insured at specified locations.

The endorsement allows for the inclusion of any person or organization listed in the schedule section. This inclusion is contingent on the liability arising from your acts or omissions or those of individuals acting on your behalf during the performance of operations for the additional insured.

Yes, coverage for additional insureds is limited. It only applies to the extent permitted by law and cannot exceed the coverage required by any contract or agreement. Additionally, the endorsement specifies that coverage is not applicable after all work has been completed or when the work has been put to its intended use by anyone other than another contractor or subcontractor engaged in the same project.

If coverage for the additional insured is mandated by a contract, the insurance provided will not exceed what is stipulated in that contract. The maximum amount payable on behalf of the additional insured will be the lesser of the amount required by the contract or the available limits of insurance.

No, this endorsement does not increase the applicable limits of insurance. The coverage provided to additional insureds remains within the existing limits of the policy.

The endorsement includes additional exclusions. It does not cover bodily injury or property damage that occurs after all work on the project has been completed or when the portion of your work that caused the injury or damage has been put to its intended use.

To ensure proper listing, include the names of the additional insureds and the locations of covered operations in the schedule section of the endorsement. If this information is not provided, it will need to be specified in the Declarations of the policy.

The CG 20 10 07 04 Liability Endorsement form is an important document in the realm of commercial general liability insurance. It serves to add additional insured parties, such as owners, lessees, or contractors, to a policy. This endorsement is often used alongside several other forms and documents that help clarify coverage and obligations. Below is a list of related documents that may accompany the CG 20 10 07 04 form.

Understanding these documents and their purposes can help ensure that all parties are adequately protected and that compliance with insurance requirements is maintained. This knowledge is essential for anyone navigating commercial contracts and liability issues.

Roof Inspection Reports - The city, state, and zip code of the structure are recorded here.

Progressive Insurance Logo Png - Contains important instructions for reporting accidents.

When engaging in a transaction involving an all-terrain vehicle, it is important to properly complete the California ATV Bill of Sale form. This document serves as a vital record for both parties and can be obtained online, such as at https://mypdfform.com/blank-california-atv-bill-of-sale/, ensuring that all necessary information is accurately captured to protect their interests during the sale or transfer process.

96 Well Plate Diagram - Perfect for both academic and industrial research settings.

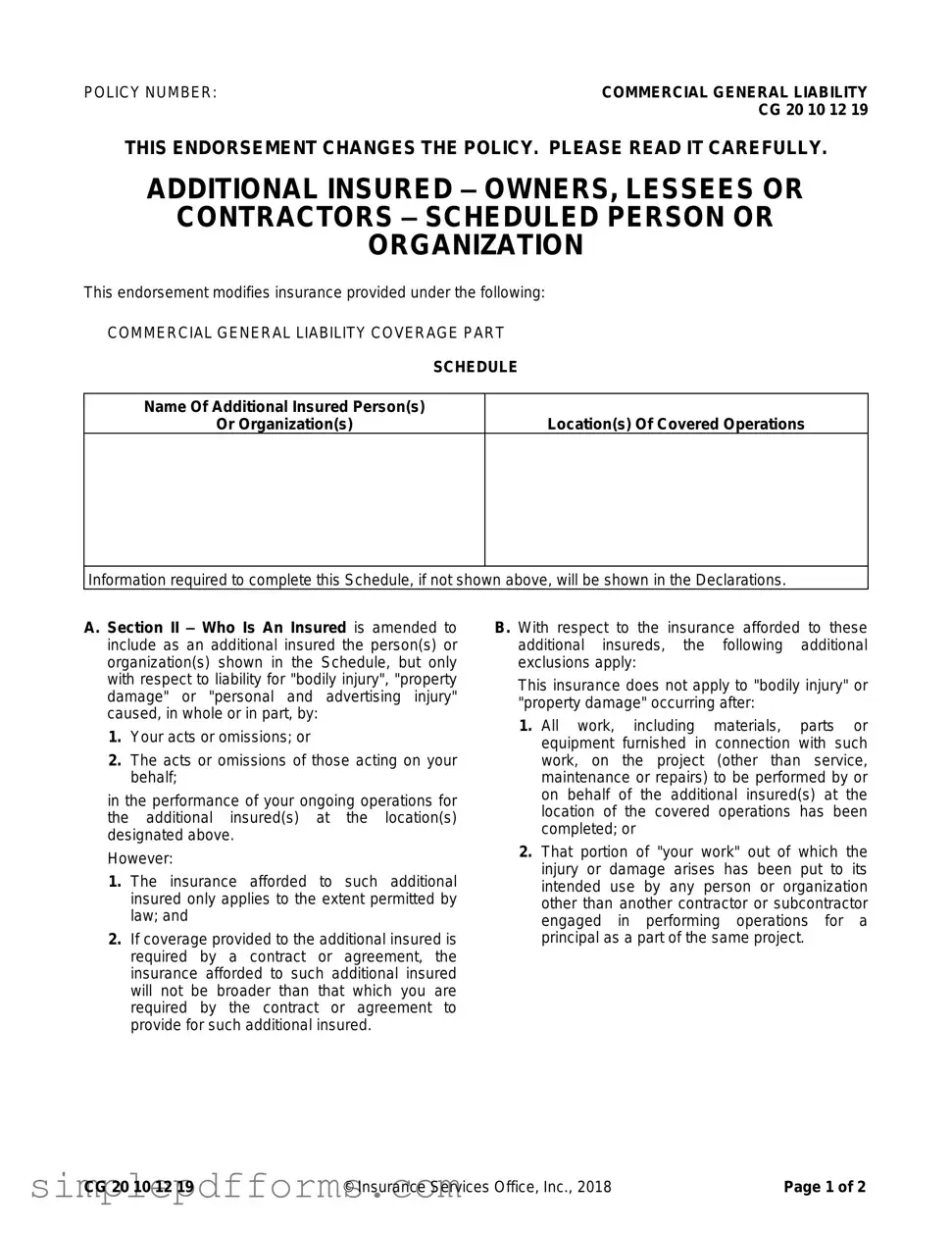

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |