Attorney-Verified Deed in Lieu of Foreclosure Document for California State

Simple PDF Forms

Attorney-Verified Deed in Lieu of Foreclosure Document for California State

Understanding the California Deed in Lieu of Foreclosure can help homeowners navigate difficult financial situations. However, several misconceptions can cloud judgment and lead to poor decisions. Here are five common misconceptions:

Awareness of these misconceptions can empower homeowners to make informed choices regarding their financial futures. It is always advisable to seek professional advice tailored to individual circumstances.

Once you have gathered the necessary information and documents, you can proceed with filling out the California Deed in Lieu of Foreclosure form. This form allows you to transfer ownership of your property back to the lender, helping you avoid the lengthy foreclosure process.

After completing the form, you will need to submit it to your lender. They will review the document and initiate the next steps in the process. Make sure to follow up with them to confirm receipt and discuss any further actions required.

Filling out a California Deed in Lieu of Foreclosure form can be a daunting task, especially when emotions are running high. One common mistake people make is not fully understanding the implications of the deed. A deed in lieu of foreclosure transfers ownership of the property back to the lender, but it also can have significant effects on credit scores and future borrowing potential. It’s essential to grasp what you’re agreeing to before signing on the dotted line.

Another frequent error is failing to provide accurate information. This includes not listing the correct property address or misrepresenting the loan details. Inaccuracies can delay the process or even lead to legal complications down the line. Double-checking all entries ensures that the form reflects the true circumstances surrounding the property and the loan.

Many individuals overlook the importance of including all necessary documentation. Alongside the deed, lenders often require additional paperwork, such as a financial statement or a hardship letter. Neglecting to submit these documents can result in the lender rejecting the deed in lieu of foreclosure. It’s crucial to gather all required materials to facilitate a smoother process.

Lastly, people often forget to consult with a legal or financial professional before proceeding. While it might seem like an unnecessary step, getting expert advice can help clarify any uncertainties and ensure that all aspects of the deed are understood. Taking this precaution can prevent costly mistakes and provide peace of mind during a challenging time.

| Fact Name | Details |

|---|---|

| Definition | A Deed in Lieu of Foreclosure allows a homeowner to transfer property ownership to the lender to avoid foreclosure. |

| Governing Law | This process is governed by California Civil Code Section 2943. |

| Eligibility | Homeowners must be facing financial hardship and unable to continue mortgage payments to qualify. |

| Benefits | It can help homeowners avoid the lengthy foreclosure process and may have less impact on credit scores. |

| Process | The homeowner must negotiate with the lender and complete the necessary paperwork to finalize the transfer. |

A Deed in Lieu of Foreclosure is a legal agreement where a homeowner voluntarily transfers the title of their property to the lender to avoid foreclosure. This process allows the homeowner to walk away from their mortgage obligations while the lender takes possession of the property.

Homeowners facing financial hardship and unable to keep up with mortgage payments may be eligible. Lenders typically require that the homeowner is in default or at risk of defaulting on the mortgage. Additionally, the property must be free of liens other than the mortgage being addressed.

This option can help homeowners avoid the lengthy foreclosure process. It may also minimize the impact on their credit score compared to a foreclosure. Furthermore, it can provide a cleaner exit from the property, allowing homeowners to move on more quickly.

Yes, there can be drawbacks. Homeowners may still face tax implications if the lender forgives any remaining debt. Additionally, this option may not be available if there are other liens on the property. It is essential to consider all consequences before proceeding.

The homeowner must first contact their lender to express interest in a Deed in Lieu of Foreclosure. The lender will then review the homeowner’s financial situation. If approved, both parties will sign the deed, transferring ownership of the property to the lender.

Homeowners will typically need to provide financial statements, a hardship letter explaining their situation, and any relevant property documents. The lender may also require additional paperwork to finalize the agreement.

In some cases, yes. If the lender does not forgive the remaining balance of the mortgage, the homeowner may still be liable for that amount. It is crucial to negotiate the terms with the lender to understand any potential liabilities.

While a Deed in Lieu of Foreclosure is generally less damaging than a foreclosure, it can still negatively impact your credit score. The exact effect will depend on your overall credit history and how the lender reports the deed to credit agencies.

Yes, it is highly recommended to seek legal advice before moving forward with a Deed in Lieu of Foreclosure. A legal professional can help you understand your rights, obligations, and the implications of this decision.

When navigating the complexities of real estate transactions, particularly those involving a deed in lieu of foreclosure, several additional forms and documents may be necessary. These documents help clarify the agreement between parties and ensure that all legal requirements are met. Below is a list of commonly used forms that accompany the California Deed in Lieu of Foreclosure.

Understanding these documents can empower homeowners and lenders alike, making the transition smoother and more transparent. Each form plays a vital role in the process, ensuring that all parties are informed and protected throughout the transaction.

Deed in Lieu of Foreclosure Pennsylvania - A deed in lieu can sometimes allow the borrower to walk away without owing additional money.

The Wisconsin Motor Vehicle Bill of Sale is essential for anyone looking to buy or sell a vehicle, as it documents the transfer of ownership clearly and effectively. To facilitate this process, you can find the necessary form at pdftemplates.info/wisconsin-motor-vehicle-bill-of-sale-form, which will help ensure all relevant details are properly recorded and the transaction proceeds without any issues.

Foreclosure Deed - A good faith negotiation between borrower and lender can lead to a successful Deed in Lieu of Foreclosure.

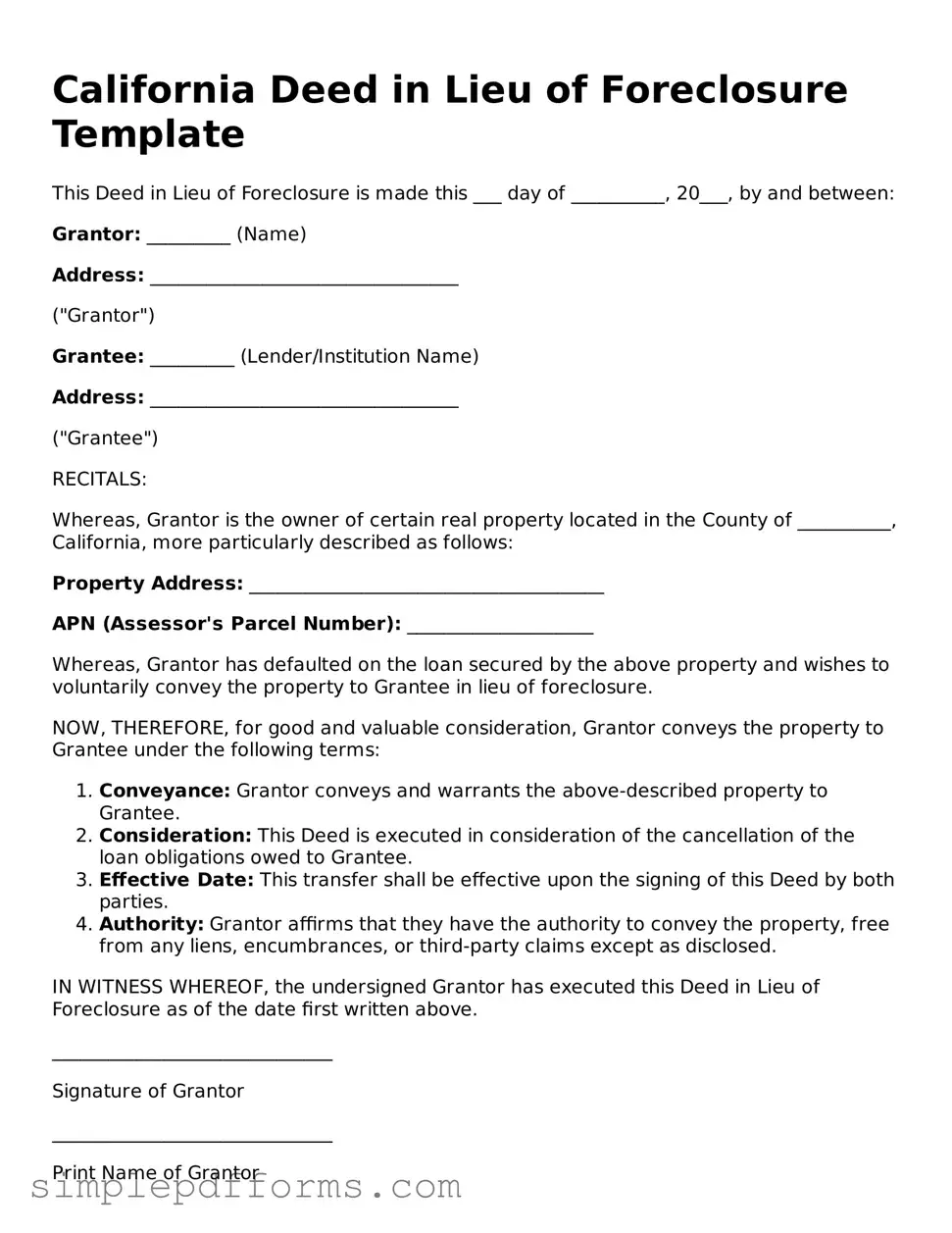

California Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is made this ___ day of __________, 20___, by and between:

Grantor: _________ (Name)

Address: _________________________________

("Grantor")

Grantee: _________ (Lender/Institution Name)

Address: _________________________________

("Grantee")

RECITALS:

Whereas, Grantor is the owner of certain real property located in the County of __________, California, more particularly described as follows:

Property Address: ______________________________________

APN (Assessor's Parcel Number): ____________________

Whereas, Grantor has defaulted on the loan secured by the above property and wishes to voluntarily convey the property to Grantee in lieu of foreclosure.

NOW, THEREFORE, for good and valuable consideration, Grantor conveys the property to Grantee under the following terms:

IN WITNESS WHEREOF, the undersigned Grantor has executed this Deed in Lieu of Foreclosure as of the date first written above.

______________________________

Signature of Grantor

______________________________

Print Name of Grantor

______________________________

Date

______________________________

Signature of Grantee

______________________________

Print Name of Grantee

______________________________

Date

This Deed is governed by the laws of the State of California and takes effect upon completion of the signing by both parties.